The consumer price index for groceries has risen more than the overall price index since the start of the pandemic, with a particularly large jump in 2022. In looking for explanations, a starting place is the behavior of raw commodity prices, which surged from early 2021 to mid-2022. In addition, wages for low-paid grocery workers have gone up faster than wages for the workforce as a whole. Finally, even though profit margins for grocery stores have gone up, the increase appears to be only a small contributor to the rise in food prices relative to the increase in their operating costs. This analysis suggests that the significant moderation in food inflation since the start of 2023 is due to still-high wage inflation for grocery workers being offset by the retreat in commodity prices.

The Volatility of Commodity Prices Is Important in Extremes

The consumer price index for food-at-home has been on a wild ride. The index was essentially unchanged in the five years before the pandemic, then rose 4 percent over the course of 2020, 6 percent in 2021, and 12 percent in 2022. The pace of annual increases then fell to 1 percent starting in 2023, but the damage to consumers was done, with the index up 25 percent from the fourth quarter of 2019 to the first quarter of 2023. For comparison, both the core goods index and the core services index were up 15 percent over this period. (“Core” refers to indexes that exclude food and energy prices.)

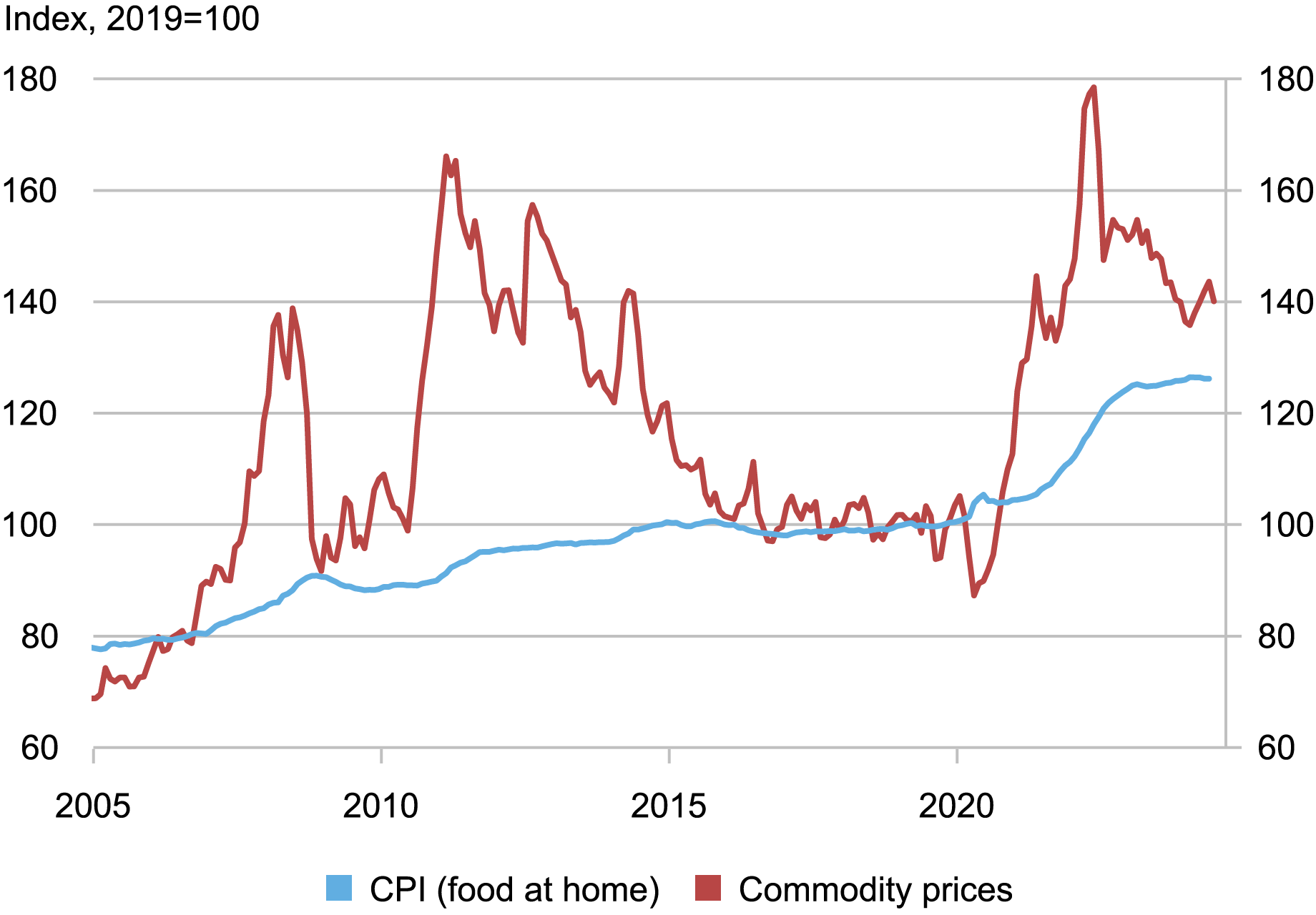

This examination of what drove prices higher starts with commodity prices. The chart below plots the S&P Goldman Sachs index for agriculture and livestock commodities and the food-at-home index. The indexes are both set to 100 in 2019. Looking at the whole period shows that grocery prices seem to only respond noticeably when commodity prices make big moves, like the jumps in 2008 and 2011 and the collapse in 2015. The rationale is that there are many other input costs dictating food prices so it takes unusual swings in commodity prices to affect grocery prices.

To see how commodity prices connect to food prices, note that the food-at-home index grew at an average pace of around 2 percent in the twenty years before the pandemic. With higher commodity prices, peak year-over-year increases hit 8 percent in 2008 and 6 percent in 2011. The subsequent retreat in commodity prices helps explain why the food index was unchanged from the end of 2014 to the beginning of the pandemic.

Big Moves in Commodity Prices Affect Grocery Prices

Sources: Bureau of Labor Statistics; S&P GSCI Agriculture and Livestock index.

Note: Commodity prices are measured by the S&P GSCI Agriculture and Livestock Index.

It is important to note that the 2020-22 surge in the food index is bigger than past similarly large increases in commodity prices. We next consider other cost factors behind food prices, specifically wages.

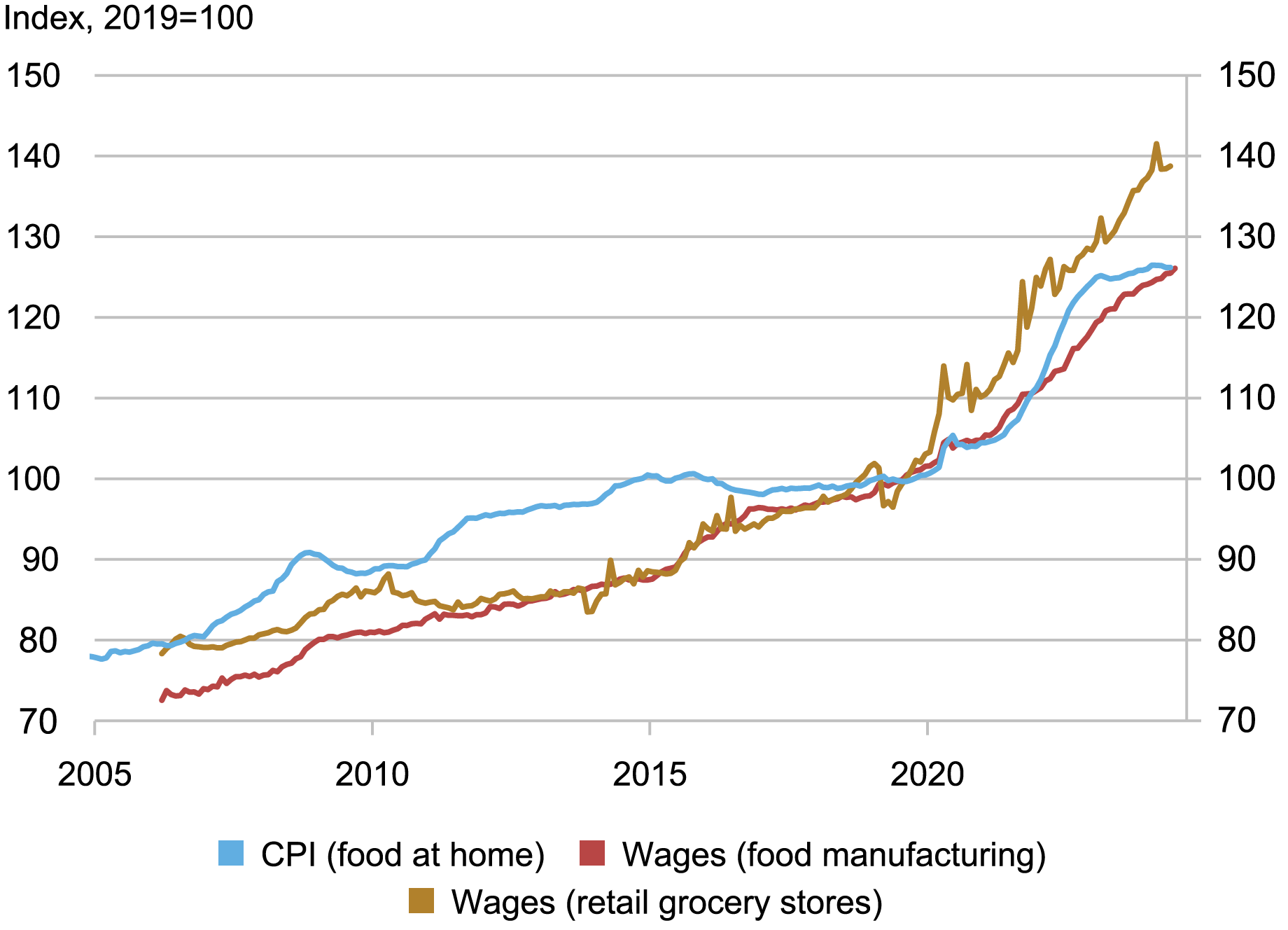

Relatively Large Wage Increases for Grocery Workers

Wages throughout the economy have gone up substantially since the start of the pandemic. The chart below presents average hourly wages for workers in the food manufacturing/processing industry and for grocery store workers along with the food-at-home index, with 2019 again set to 100 for each series. Consumer prices and wages in the two food sectors have tended to move in sync, except during periods of large commodity swings, as seen in the first chart. That is, food-at-home prices rose faster than these wages in 2008 and 2011 and increased at a slower pace than wages in the 2015-19 period.

What sticks out in the chart is the rise in wages for retail grocery workers since the start of the pandemic. The increase in these workers’ wages since 2019 has been roughly 15 percentage points greater than that of wages for the food manufacturing sector and the workforce as a whole. Grocery worker wages would seem then to be a key factor in why the food index has gone up more than the core price index. Note, though, that these workers are still in low-pay jobs, currently earing $13 an hour less than the private-sector average ($21.60/hour in the first quarter of 2024 versus $34.60/hour) according to payroll employment data.

Wages for Grocery Workers Are Up Sharply

Source: Bureau of Labor Statistics.

Note: Wages are average hourly wages.

An open question is whether grocery inflation can stay as moderate as it has been since early 2023 with grocery worker wage inflation still elevated. Specifically, food manufacturing wages rose 4 percent and grocery workers’ wages rose 6 percent year-over-year in May 2024, while the food-at-home index rose by 1 percent.

Profit Margins Haven’t Been Important

There has been some speculation that increases in profit margins helped push up inflation during the pandemic. The Quarterly Financial Report put out by the Census has data for revenues and operating costs from a survey of corporations in the food sector. There is a caveat to using this data set since the revenue for these firms rose at a slower pace than recorded in the corresponding retail sales data, which is a broader survey measure. Nevertheless, it does offer insights from looking at the evolution of operating cost, revenues, and profit margins of the surveyed firms.

In the case of food manufacturers, operating costs (wages, commodity goods, energy, other inputs) in 2023 were up 15 percent relative to what they were in 2019, while costs for food and beverage retail stores increased 18 percent. Revenues rose 15 percent and 20 percent, respectively. For comparison, retail sales data recorded a 25 percent increase in revenue for food and beverage stores.

Putting these results together yields a measure of the profit margin: the ratio of revenue minus operating costs to revenue. For food manufacturing, the margin was little changed, going from 6.9 percent in 2019 to 6.8 percent in 2023, while increasing from 2.9 percent to 4.4 percent for food and beverage retail stores. But put in context, this increase in grocery store profit margins (revenues over costs) is small compared to the 25 percent increase in grocery prices over this period.

To be sure, profits in dollar terms have gone up substantially. Indeed, the operating profits of the surveyed food and beverage retail stores rose from $14 billion in 2019 to $25 billion in 2023, a 79 percent increase. The jump reflects a higher profit margin applied to a higher level of operating expenses. Again, this roughly $10 billion increase in operating net income is marginal relative to the $100 billion increase in revenues reported by these firms.

Putting these factors together suggests that the unusually high food inflation experienced in the first three years of the pandemic appears to have been due, in part, to much higher food commodity prices and large increases in wages for grocery store workers. The subsequent drop in commodity prices then helped bring food inflation down below the core inflation rate even though heightened wage pressure for grocery workers continued. In the end, the moderation of food price inflation has caused the gap that developed between the food index and the core index since the start of the pandemic to shrink from 10 percentage points at the end of 2022 to 5 percentage points in June 2024.

Thomas Klitgaard is an economic research advisor in International Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Thomas Klitgaard, “What Was Up with Grocery Prices?,” Federal Reserve Bank of New York Liberty Street Economics, July 16, 2024, https://libertystreeteconomics.newyorkfed.org/2024/07/what-was-up-with-grocery-prices/.

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

Source link